The saving of money is usually more critical than spending big. It is with this in mind that the State Bank of India (SBI) has launched the Har Ghar Lakhpati Scheme which is a recurring deposit scheme that aims at enabling common people to accumulate an appreciable savings corpus through minimum monthly deposits.

The scheme is disciplined saving based and provides guaranteed returns, which makes it a good choice among risk-averse investors who do not want to take risks with the market.

What Does the SBI Har Ghar Lakhpati Plan Entail?

The Har Ghar Lakhpati Scheme is a recurrent deposit (RD) that is a goal-based scheme provided by SBI. Under this strategy, the customers will open an amount of money on a fixed monthly deposit with a chosen tenure and the bank will pay interest on the deposits. Upon maturity the investor is given a lump sum ranging up to 1 Lakh or even more depending on the investment period and the monthly contributions.

This scheme has guaranteed returns unlike the mutual funds or products based on equity and thus it is recommended to the conservative savers, those with salaries and the first time investors.

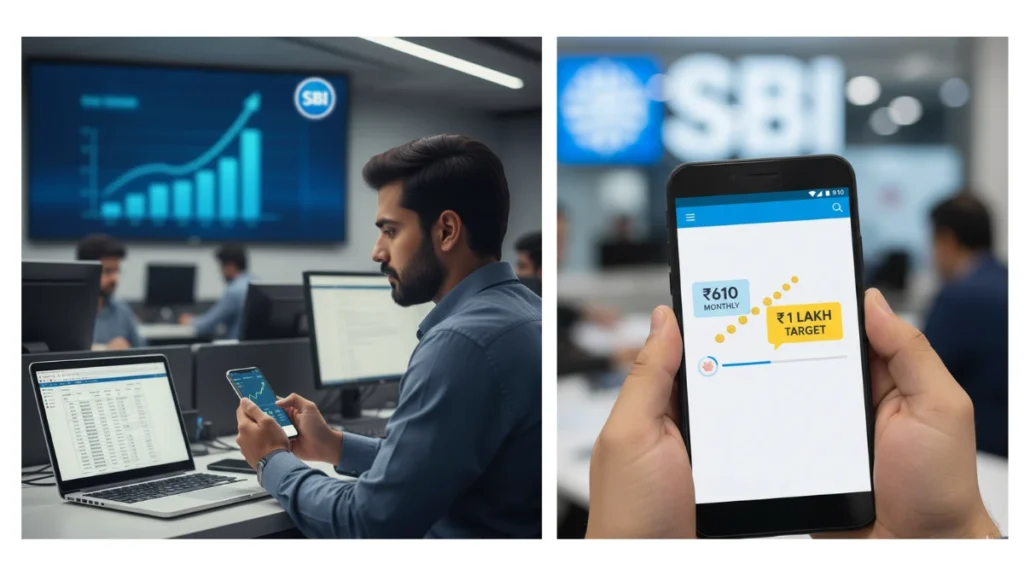

How a ₹610 Monthly Investment Can Turn Into ₹1 Lakh

The affordability of the scheme has been one of the most discussed features. SBI calculations show that:

- Through an investment of approximately 10 years with a sum of 1000 to invest, an investor will have an approximate sum of 1 lakh at maturity by investing approximately Rs.610 per month.

- That is a saving of less than 25 a day, which is just a reminder that small and regular contributions to the savings account can have a huge long-term effect.

The program would promote a savings culture among the households without straining their monthly financial limits.

Interest Rates Offered Under the Scheme

The returns on the Har Ghar Lakhpati RD scheme will be determined by the tenure and type of customer:

- The general customers are given an interest rate that ranges between 6.30 and 6.55 percent per annum.

- The rates are higher to senior citizens who get it up to 7.05% per annum on some tenures.

Depending on the policy and current market conditions by SBI, interest rates are liable to change yet the returns are stable and secure.

Flexible Tenure Options for Faster Growth

To the individual who wishes to achieve the ₹1 lakh goal at a lesser time, SBI will have lesser deposits with a reduced monthly deposit:

- 3 years: Around ₹2,500 per month

- 4 years: Around ₹1,800 per month

- 5 years: Around ₹1,400 per month

This is flexible so that investors can have a plan depending on their level of income and targeted objectives of their finances.

No 1 Lakh limit: Increased Savings Goals

Although the scheme is commonly referred to as ₹1 lakh target, it is not limited to such an amount among the investors. SBI gives a chance to its customers to have higher maturity, 2 lakh, 3 lakh and above. Deposits to be made will also vary automatically based on the selected goal and term chosen by the bank.

This renders the scheme appropriate in planning the costs involved in raising the children, weddings, emergency funds or future purchases.

Who is eligible to open an SBI Har Ghar Lakhpati account?

The scheme is open to a vast number of customers:

- The holders of individual and joint accounts.

- Minors Parents or guardians who open accounts on behalf of the minor.

- Children aged more than 10 years (can sign) with supervision.

It is possible to open accounts at the branches of SBI and upon the choice of digital banking channels.

Why this Plan is attractive to Indian Families

The reason is that the Har Ghar Lakhpati Sbi Scheme is simple, safe, and cheap. This RD plan has clarity and peace of mind at a time when most of the investment choices are associated with risks and complicated terms.

It is especially useful when individuals need to get fixed returns and have no desire to follow markets or to invest their money and watch changes.

Final Takeaway

The scheme of Har Ghar Lakhpati by SBI is a demonstration that large investment is necessary to accumulate wealth. Having monthly savings under discipline and a long-term view, even small deposits can reach a significant financial relief.

Investors however are advised to weigh their financial requirements and compare the alternatives before they commit particularly when their interest is creating wealth in the long run or beating inflation.

Disclaimer: This article is for informational purposes only. Interest rates and returns are subject to change. Readers should consult a financial advisor before investing.