Salesforce First-Quarter Sales: Salesforce (NYSE: CRM) was the ultimate poster child for growth-at-all-costs tech investing. But as the enterprise software market matures, the company is attempting one of the trickiest balancing acts in tech: shifting from hyper-growth to a highly efficient cash machine.

Its recent fiscal first-quarter earnings report has ignited a fierce debate on Wall Street. While the software giant successfully showed off widening profit margins, an unmistakable deceleration in its long-term growth engine is causing some investors to pump the brakes.

Let’s break down the data to see where the company actually stands, what’s driving the numbers, and why the market is pricing the stock the way it is.

Salesforce First-Quarter Sales Big Picture: By the Numbers

Salesforce kicked off the first quarter of its new fiscal year by delivering total revenue of $11.1 billion, up from the $9.8 billion it recorded during the same period last year. On the bottom line, basic earnings per share (EPS) jumped to $2.43, a notable step up from $1.61 a year ago.

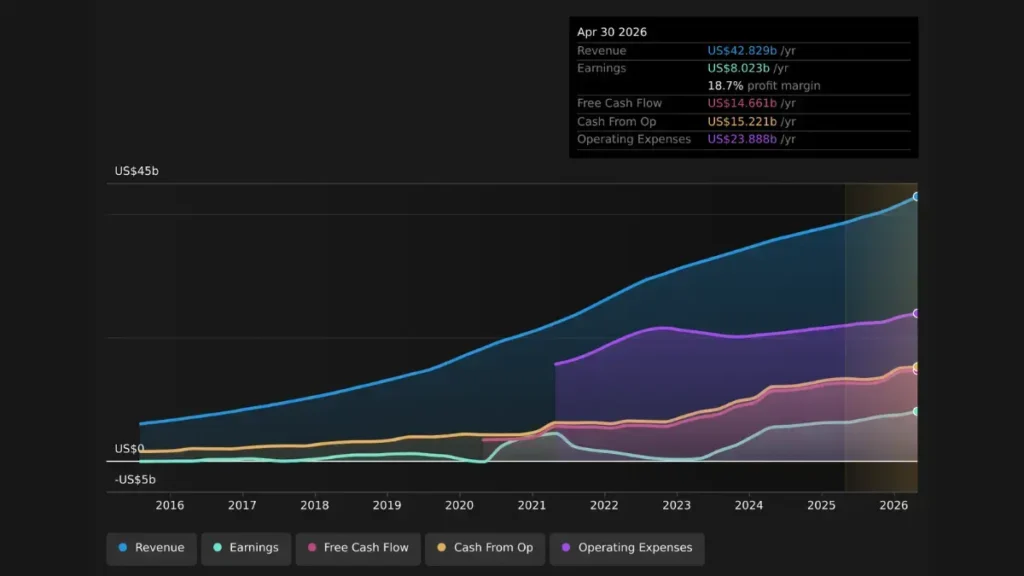

Zooming out to look at the trailing 12 months, Salesforce pulled in a staggering $42.8 billion in total revenue, translating to a full-year basic EPS of $8.65.

On the surface, these are massive headline numbers. However, beneath the hood, investors are looking past the raw volume to evaluate the structural quality of Salesforce’s remaining runway.

The Bull Case: The Margin Engine is Firing

If you talk to Salesforce bulls, their excitement centers almost entirely on efficiency. Over the past year, the company converted its $42.8 billion revenue base into $8.0 billion in pure net income.

This means its trailing net profit margin now sits at 18.7%, up significantly from the 16.1% it logged the year prior.

What’s Driving This? This margin expansion is proof that management’s aggressive pivot toward operational discipline and AI automation is working. By leaning into platforms like Data Cloud and its newly deployed Agentforce autonomous bots, Salesforce is proving it can lower its own cost of doing business, extracting more profit out of every single dollar it brings in.

Looking down the road, Wall Street analysts project that Salesforce can scale these net margins to roughly 19.8% by 2029. The current trajectory shows that the company is well on its way to hitting those long-term profitability milestones.

The Bear Case: A Structural Growth Slowdown

Despite the highly profitable quarter, conservative analysts are pointing out clear signs of structural fatigue in Salesforce’s core business model.

While the company posted a 29.3% earnings growth rate over the past year—a number most traditional companies would kill for—it marks a sharp drop from its five-year historical average of 37.5% per year. The core customer relationship management (CRM) software market is highly saturated, meaning Salesforce can no longer rely on easy domestic market expansion to fuel its historical growth rates.

Even more telling are the forward-looking estimates. Future projections suggest that Salesforce’s long-term earnings growth will settle into a much quieter 9.5% annual rate over the next few years, alongside an annual revenue growth forecast of 8.6%.

When you compare that 9.5% earnings growth to the broader U.S. stock market’s projected average growth rate of 17%, it becomes clear that Salesforce is transitioning from a high-flying growth stock into a mature, stable tech giant.

The Valuation Disconnect: Is the Stock Cheap?

The most compelling aspect of Salesforce right now isn’t the earnings report itself—it’s how the public market is pricing the stock in response to it.

Trading around $176.17, Salesforce currently carries a trailing price-to-earnings (P/E) multiple of 18x. For an enterprise software titan, that is an incredibly low number.

To put that multiple into perspective, consider its peers:

- Direct Software Competitors: 59.8x average

- Broader U.S. Software Industry: 28.5x average

Because of the single-digit revenue growth forecasts, Wall Street has aggressively compressed Salesforce’s valuation. Yet, according to fundamental Discounted Cash Flow (DCF) models, the stock’s intrinsic fair value sits closer to $237.91, while Wall Street’s consensus target price remains at $257.73.

This leaves investors with a classic market puzzle. Is Salesforce a value trap because its hyper-growth days are behind it? Or is it a rare, high-margin bargain hiding in a historically expensive tech sector?

Salesforce (NYSE:CRM) Financial Scorecard

| Key Metric | Current Performance | Benchmark / Historical Context |

| Q1 Revenue | $11.1 Billion | $9.8 Billion (Same Quarter Last Year) |

| Trailing 12-Month Revenue | $42.8 Billion | Massive scale, but top-line growth is slowing |

| Net Profit Margin | 18.7% | 16.1% (Prior Year Average) |

| Past Year Earnings Growth | 29.3% | 37.5% (Company’s 5-Year Average) |

| Expected Future Growth | ~9.5% Per Year | 17.0% (Broader U.S. Market Average) |

| Trailing P/E Ratio | 18x | 28.5x (Software Industry Average) |

Disclaimer: This article is intended entirely for informational and educational purposes. It should not be taken as financial, investment, or legal advice. Always perform your own due diligence or consult with a certified financial professional before making investment decisions.